Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Gardner Report – Q3 2019

The following analysis of the Metro Denver & Northern Colorado real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere real estate agent.

ECONOMIC OVERVIEW

Colorado’s economy picked up, adding 64,900 new non-agricultural jobs over the past 12 months — a growth rate of 2.4%. Over the past three months, the state added an impressive 28,300 new jobs.

In August, the state unemployment rate was 2.8%, down from 3.4% a year ago. Unemployment rates in all the counties contained in this report were lower than a year ago. It is fair to say that all markets are now at full employment.

HOME SALES

- In the third quarter of 2019, 17,562 homes sold. This is an increase of 5.1% compared to the third quarter of 2018 but 1.6% lower than the second quarter (which can be attributed to seasonality). Pending sales — a sign of future closings —rose 9.7%, suggesting that closings in the final quarter of 2019 are likely to show further improvement.

- Seven counties contained in this report saw sales growth, while four saw sales activity drop. I am not concerned about this because all the markets that experienced slowing are relatively small and, therefore, subject to significant swings.

- I was pleased to see an ongoing increase in the number of homes for sale (+16.9%), which means home buyers have more choice and feel less urgency.

- Inventory levels are moving higher, and demand for housing appears to be quite strong. As I predicted last quarter, home sales rose in the third quarter compared to a year ago.

HOME PRICES

- Home prices continue to trend higher, with the average home price in the region rising 3.8% year-over-year to $477,776.

- Interest rates are at very competitive levels and are likely to remain below 4% for the balance of the year. As a result, prices will continue to rise but at a more modest pace.

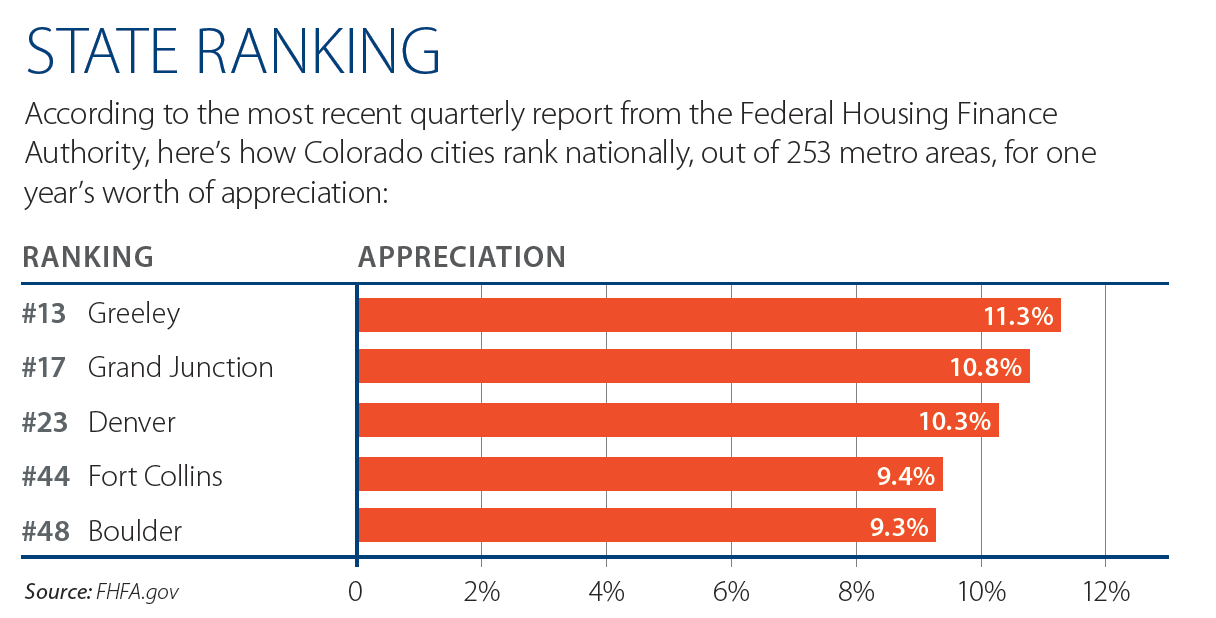

- Appreciation was again strongest in Park County, where prices rose 7.8%. We also saw strong growth in Weld County, which rose 7.4%. Home prices dropped in Clear Creek County, but, as mentioned earlier, this is a small market so I don’t believe this is indicative of an ongoing trend.

- Affordability remains an issue in many Colorado markets and this will act as a modest headwind to ongoing price growth.

DAYS ON MARKET

- The average number of days it took to sell a home in the markets contained in this report rose seven days compared to the third quarter of 2018.

- The amount of time it took to sell a home rose in all counties compared to the third quarter of 2018.

- It took an average of 30 days to sell a home in the region — an increase of 1 day compared to the second quarter of this year.

- The Colorado housing market is still performing well, and the modest increase in the length of time it took to sell a home is a function of greater choice in homes for sale and buyers taking a little longer to choose a home.

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

For the third quarter of 2019, I continue the trend I started last summer and have moved the needle a little more in favor of buyers. I continue to closely monitor listing activity to see if we get any major bumps above the traditional increase because that may further slow home price growth. However, the trend for 2019 will continue to be a move toward a more balanced market.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

When It Comes Time to Downsize

When it comes time to decide if you want to downsize, there are many thoughts and emotions that go speeding through your mind. Maybe you have already decided this is your home for the rest of your life. Your home was the perfect place to meet your needs when you were in an earlier cycle of life, and will be the ideal home for all the events you see happening in your next. If you are inclined to feel that the home you currently reside in may have out-lived its purpose, you may be struggling with some of the same thoughts and emotions my husband and I had when it came to the emotional and financially sensitive decision to downsize.

In our situation, we loved our home. It provided everything we needed to raise our three children, plus nurture all the creative projects that identified who we are as a family as well as individuals. Our children were just like anyone else’s; loved, individually different, all requiring unique activities and space to help them grow, using their special talents. We loved our neighborhood and took an active part in making it an extension of our home. Considering that it had been our home for decades, deciding to leave was emotionally difficult.

We spent several years before we knew we would leave our home, looking at all the smaller options. We wondered, should we look for another single-family dwelling or check out other options like co-ops of condominiums? My husband had spent the past twenty-five years mowing our lawn and was quite willing to remove this task from his plate. I, on the other hand, still loved to garden. Was there a living environment that could satisfy both these expectations? We looked at every condominium and every co-op in the Seattle area for five years, but nothing really fulfilled everything we needed. We had a list of features including a garden spot, closets and efficient use of space, etc. I’m an Old World Charm lady, but guess what? Back in the 20’s ladies only owned three dresses. Let’s just say, I own a few more outfits than most pre-war closets were meant to hold. So the search went on.

When our children finally reached their 20’s and my husband wanted to retire, we knew it was time to make our move. Like I said, everyone loves their children, but not all the party time we now came to expect in our rec room every weekend. We were ready to have a space of our own, and it was time for our kids to begin their next cycle in-life. We also had too much of our finances tied up in a 3,000 square foot house, when in reality we needed less and could save more. We had to leave the home we had dedicated to making our unique expression of who we were, and leave very soon.

If any of this sounds familiar, your task will be a little easier than it seems! Here is some practical advice for making your move:

Define your needs: Narrow down your ideal needs. Start by deciding if you want a single-family versus multi-family dwelling. Consider your price range, and then space needs.

Downsize: We downsized a bit more than we should have, but we sure got rid of lots of items we collected over the past 25 years. Some of them were special to me. I’d purchased a beautiful wood serving tray at a yard sale with one of my dearest friends. I had to borrow money from her to buy it. I solved the problem by giving it to her when we moved, and I still see it when I visit her home. My children took much of the furniture they had a special connection to, and my nephew, who spent nearly every Christmas sitting in his favorite red chair, can now enjoy it in his own home.

Let go: Leaving the neighborhood and all our lifelong friends was the most difficult process, I think, of all the decisions we had to make. We still see them, but as I’m writing this my eyes are tearing up. It’s hard to re-visit my old neighborhood and see my old home cared for in a different way than I had lovingly done for twenty-five years. But it does give us plenty of things to talk about with old friends when we get together.

What did we end up doing? We moved into a vintage 1930’s co-op in a walkable part of town. I have just the right amount of gardening space that I share with other owners. We have made wonderful friends with some of our neighbors and get together frequently for happy hour and spur-of-the-moment gatherings. It’s a different lifestyle than we had before but, believe me, there are plus sides. In no way will any of our three wonderful, adored, adult children ever be able to move back home, since we now live in an 850-square-foot co-op with every space used on a daily basis. There were times when I wouldn’t go in one of my rooms in our old home for several weeks. This is not a problem now. Yes, maybe it’s too small, but we can always move into a larger place if and when we feel it’s time.

What are your questions about downsizing your home? What features do you require to live in a smaller, more efficient dwelling?

Pat Eskenazi is a Windermere veteran, working in marketing for the past 12 years. She has lived in Seattle since 1952. Her favorite place to walk is along Golden Gardens, and she especially loves to climb the stairs up to the Sunset Hill neighborhood where she lived with her 3 children and husband for 25 years.

The Reality of Home Improvement: HGTV Installment

On any given weekend in my house, at least a couple of hours will be spent watching the designers, craftspeople and entertainers on HGTV or its spunky sister station, the DIY Network. The premise of these home-centered television networks is that somewhere, sandwiched between long commercial breaks for paint, faucets, flooring warehouses and something called “Slab Jacking”, you’ll find programming about real people making real decisions about their homes. Sometimes those decisions are about buying a home, while other times they may be about selling or remodeling a home. In all of the situations, experts are brought in to help and a camera crew just happens to tag along, so the rest of us can enjoy the unfolding drama from the comfort of our couches.

Home improvement programming has been around for a long time and is generally considered reality TV, but a lot of the real life is lost between cuts. Here’s a quick guide of some of the more popular programs.

House Hunters – The formula is simple but always entertaining. Each episode begins with someone unhappy with their living situation, so they call an agent and look at 3 properties. After weighing the options, a home is chosen. Of course, this show is over-simplified and leaves out the long weekends the buyer spends in their agent’s car driving from listing to listing. What you do get is a sense of home values and styles in different regions, the humor of buyers’ reactions to homes, and the excitement new home owners feel as they take the keys to their dream home. You rarely get the type of tension home shopping can bring. The big climax of the show is when an offer is made: the narrator might say something like, “Though their offer was rejected the first time around, the other buyer ultimately backed out and they ended up getting the house for X amount.” But I don’t think they usually talk about it at all. For that kind of tension, you need to check out Property Virgins. The best part of the half hour happens in the last 30 seconds when you see how the new owner redecorates the home in their own style.

Property Virgins– Similar premise to House Hunters, except these first-time homebuyers walk through the basics. The best part about the show is the excitement (and sometimes clumsiness) of the virgin house-hunters. The worst part of this show is when would be homebuyers have unrealistic expectations for their first home.

House Hunters International – Comparable to House Hunters but everyone has accents and the kitchens are shockingly small.

Designed to Sell – Did you know that your spare bedroom filled with Grandpa’s taxidermy and the vintage 1950’s kitchen can be a turn-off to potential buyers? Valuable lessons like these are a just a few of the gems I’ve picked up on Designed to Sell. Each episode features a home which has been racking up days on the market but no one is interested in buying. That’s where the army of carpenters and designers step in. When they’re done, the house that looked like Grandma’s musty basement now looks like the lobby of a hip hotel, and they only spent a few hundred dollars. I love this program for the inspiration but find it short on reality. The listed prices of these improvements don’t seem realistic, and I often wonder if the costs include the lifetime of carpentry skills, design training, garage filled with power tools and time required to do the job. If you are looking for design ideas and hope for a home that isn’t attracting buyers, you’ll find some great ideas here, but take the true cost of those improvements with a grain of salt.

Real Estate Intervention – Being a real estate agent takes a lot of diplomacy, and this is never more important than that moment they suggest a market-friendly price to a home seller. On Real Estate Intervention, that diplomacy generally fails, sellers are unrealistic, and a stern man with a menacing mustache steps in for an intervention. He dishes out tough love to the seller and paints a clear picture of market reality. In a half hour he is able to change minds and make the seller feel good about the decision they made.

This Old House – This PBS staple wrote the book on home improvement programming. With TOHyou’ll trade commercials for pledge drives, but you’ll also get a more cerebral home improvement viewing experience. TOH does take patience, as it takes a full season to complete a home improvement project instead of 30 minutes on other programs. If you are looking for the same quality instruction in a more digestible format, you can check out the spin off, Ask This Old House.

Be warned that the home improvement bug often bites soon after watching any of these programs. After a long HGTV bender, I find myself wandering through the paint sample aisle and making trips to home improvement stores that aren’t on my way home from the office. Sometimes life does imitate art and the voice in the back of my head keeps saying, “They make it look so easy.”

What about you? Do you find home-improvement shows useful or do you think they set unrealistic expectations? What are your favorite home-improvement resources?

by Justin Waskow

Divorce, Custody, and Employee Mobility

Divorce, child custody and relocation are all difficult topics however, knowing the facts will help you make the decisions that are right for you and your family. Below you will find an excerpt from an article recently published in Mobility Magazine by Windermere’s own Peggy Scott, GRI, CRP, GMS. She is the relocation director and designated broker for Windermere Relocation and Referral Services, Seattle, WA. You can read the article in its entirety here: http://bit.ly/9PrKxL

“As society becomes increasingly mobile, so does the frequency with which global mobility professionals encounter relocation cases involving child custody. Scott defines custody, discusses its effects on mobility, and offers a case study demonstrating how divorce affects the relocation process.”

While the divorce rate varies greatly in each country of the world, affecting the lives of men and women, those with children be affected the greatest. No family law generates more concern, strife, and emotional turmoil than child custody and visitation matters. Every court around the nation will advocate for the best interest of the children involved in divorce.

Developing an amicable parenting plan or agreement for the interests of the children is the best solution to establishing custody of a child. The best interest of the child is served by a parenting arrangement that best maintains a child’s emotional growth, health and stability, and physical care. According to Washington state law, the best interest of the child ordinarily is served when the existing pattern of interaction between a parent and child is altered only to the extent necessitated by the changed relationship of the parents.

If the parents cannot reach an agreement concerning the custody and parenting plan for the child, then the court may establish either sole or mutual decision-making authority as well as residential provisions. The parenting plan or agreement needs to support, in detail, the child’s best interest in the areas of school, physical care, traveling expenses, individual parental authority, and residence options and rules. All divorce cases involving child custody, whither uncontested or contested, must include a parenting plan or custody order (either by agreement or ordered after trial) that is adopted by the courts.

To read the rest go here: http://bit.ly/9PrKxL

Considering Becoming a Landlord? How to Evaluate Whether to Rent or Sell Your Property

Over the last few years, we have seen an increase in homeowners choosing to become landlords rather than placing their homes on the market. In deciding whether or not becoming a Landlord is right for you, there are a number of factors to consider, but primarily they fall into the following three categories: Financial Analysis, Risk and Goals.

The financial analysis is probably the easiest of the three to assess. You will need to assess if you can afford to rent your house. If you consider the likely rental rate, vacancy rate, maintenance, advertising and management costs, you can arrive at a budget. It is important both to be reasonably correct in your assumptions and to have enough reserves to cover cash-flow needs if you’re wrong. The vacancy rate will be determined by the price at which you market the property. Price too high and you’re either vacant or accepting applicants that, for some reason, couldn’t compete for more competitively priced homes. Price too low and you don’t achieve the revenue you should. If you want to try for the higher end of an expected range, understand that the cost may be a vacant month. It is difficult to make up for a vacant month.

The financial analysis is probably the easiest of the three to assess. You will need to assess if you can afford to rent your house. If you consider the likely rental rate, vacancy rate, maintenance, advertising and management costs, you can arrive at a budget. It is important both to be reasonably correct in your assumptions and to have enough reserves to cover cash-flow needs if you’re wrong. The vacancy rate will be determined by the price at which you market the property. Price too high and you’re either vacant or accepting applicants that, for some reason, couldn’t compete for more competitively priced homes. Price too low and you don’t achieve the revenue you should. If you want to try for the higher end of an expected range, understand that the cost may be a vacant month. It is difficult to make up for a vacant month.

Consider the other costs renting out your property could accrue. If you have a landscaped or large yard, you will likely need to hire a yard crew to manage the grounds. Other costs could increase when you rent your home, such as homeowner’s insurance and taxes on your property. Also, depending on tenant turn-over, you may need to paint and deal with maintenance issues more regularly. Renting your home is a decision you need to make with all the financial information in front of you. You can find more information about the hidden costs of renting here.

If your analysis points to some negative cash-flow, that doesn’t necessarily mean that renting is the wrong option. That answer needs to be weighed against the pros and cons of alternatives (i.e., selling at the price that would actually sell), and some economic guesswork about what the future holds in terms of appreciation, inflation, etc. to arrive at an expectation of how long the cash drain would exist.

Risk is a bit harder to assess. Broadly though, it’s crucial to understand that if you decide to lease out a home, you are going into business, and every business venture has risks. The more you know, the better you can mitigate those risks. One of the most obvious ways of mitigating the risk is to hire a management company. By hiring professionals, you decrease your risk and time spent managing the property (and tenants) yourself. However, this increases the cost. So, as you reduce your risk of litigation, you increase your risk of negative cash-flow, and vice versa… it’s a balancing act, and the risk cannot be eliminated; just managed and minimized.

In considering Goals, what do you hope to achieve by renting your property? Are you planning on moving back into your home after a period of time? Will your property investment be a part of your long-term financial planning? Are you relocating or just hoping to wait to sell? These are all great reasons to consider renting your home.

Keep in mind that renting your family home can be emotional. Many homeowners LOVE the unique feel of their homes. It is where their children were raised, and they care more about preserving that feel than maximizing revenue. That’s OK, but it needs to be acknowledged and considered when establishing a correct price and preparing a cash flow analysis. Some owners are so attached to their homes that it may be better for them to “tear off the band-aid quickly” and sell. The alternative of slowly watching over the years as the property becomes an investment instead of a home to them may prove to be more painful than any financial benefit can offset.

In the process of considering your financial situation, the risks associated with becoming a landlord, and the goals you hope to achieve with the rental of your property, – ask yourself these questions. Before reaching a conclusion, it’s also a good idea to familiarize yourself with the landlord-tenant-lawspecific to your state (and in some cases, separate relevant ordinances in the city and/or county that your property lies within) and to do some market research (i.e. tour other available similar rentals to see if your financial assumptions are in line with the reality of the competition across the street). If you are overwhelmed by this process, or will be living out of the region, seek counsel with a property management professional. Gaining experience the hard way can be costly.

Posted in Selling and Property Management by Windermere Guest Author

J. Michael Wilson is the dedicated broker at Windermere Property Management Seattle, and has 17 years of experience managing properties in the Seattle region.

What You Need to Know about Buying a Bank Owned Home

Recently, news about how to purchase a real-estate owned (REO/bank owned) home, foreclosure property or short sale is everywhere. Bank owned homes are sold directly from the lender after the foreclosure process is complete, and while you may save quite a bit of money by choosing to go for this type of home, it is not without trials and tribulations. The process of purchasing a home directly from a lender can be long and arduous, but could very well be worth it in the end.

If you have your sights on a particular home or are looking to find a deal on your first, working directly with the lender may be your only option. Purchasing a bank owned home is not for the faint of heart, here are some tips for negotiating the REO process:

1. Be prepared: The condition of bank owned properties is usually poor and hard to show. Past owners may have left angry and left the home in bad condition with foul smells, missing appliances, wires taken from breakers, gas fireplaces gone, even bathrooms without toilets and sinks.

2. Understand the costs: Maintenance or repairs may be necessary, since these homes have been vacant for an unknown period of time–sometimes months or years. Keep in mind, when they were occupied the owners could have been under a financial hardship, preventing them from doing regular seasonal care or repairs when needed. Remember as well that the bank is trying to sell the house immediately, so you will receive a financial break in the price rather than a willingness to negotiate on the maintenance and repair issues.

3. Accept the unknown: In traditional real estate transactions, homeowners fill out Form 17 regarding important information about the history of the house. A bank owned home is either exempt or marked with “I don’t know” throughout the document. Not having the accuracy of this 5 page disclosure form could leave you with a lot of unanswered questions on the history of the home.

4. Know what is non-negotiable: The pricing on the house may not get much lower. Some of these properties can be “a dream come true” if you get them at an amazing price, or they could be your worst nightmare. Do your due diligence researching any property, and conduct all necessary inspections to safeguard yourself. Some major repairs may be negotiable, but will likely not reduce the home price.

5. Make a clean offer: The higher the price you can offer, the better. Include your earnest money, keep contingencies to a minimum, and suggest a reasonable closing date. The simpler your offer is, the higher chance you have of the bank accepting your offer or countering in a reasonable time period.

6. Be patient: Consult with a professional who handles bank owned home purchases to help you negotiate the pathway to homeownership. The process of purchasing a bank owned, foreclosed or short-sale home is typically longer than a typical real estate sale.

What do you want to know about purchasing bank owned, foreclosure and short-sale properties?

Posted in Uncategorized by Windermere Guest Author

Tonya Brobeck is a Broker at Windermere Lake Stevens. She has a total of 17 years combined residential real estate and worldwide resort sales & marketing experience.

Investing in Home: Building a Foundation for Memories

“Of course, thanks to the house, a great many of our memories are housed, and if the house is a bit elaborate, if it has a cellar and a garret, nooks and corridors, our memories have refuges that are all the more clearly delineated. All our lives we come back to them in our daydreams.”

Gaston Bachelard, the Poetics of Space

I have been following the news about the housing market pretty closely and am pretty disappointed with some of the articles declaring a case against homeownership. I couldn’t disagree more. If anything, I see the value of homeownership: responsible financial investment, social stability and community connection as more important than ever.

I was particularly moved by the story in the Seattle Times yesterday about the Lutz family in Ballard, a family with seven adopted siblings that are helping their parents move from their family home to a smaller condo now that their children have left the nest. Though their story is far from typical, it really resonates how home is the center of family life, a place where memories are created and how houses tell the stories of the lives we build while in their shelter.

Homes do that for people. They are the places where some of our most intimate stories unfold.

Finding and creating a home is an emotional, psychological, social and financial investment. There is a lot of energy involved in finding the place to envision the future, raise a family, and perhaps retire. There is no other investment as enjoyable as your own home. Investments in gold or stocks cannot compare to the feelings about a place where you collect memories, create spaces that reflect your ideals and develop to fit your needs over time.

Beyond the emotional ties to home, a number of studies have shown that home ownership has a great impact on feelings of personal autonomy, life satisfaction and increased investment in the community. The sense of satisfaction goes beyond the ability to paint walls whatever color we want, or make improvements to our homes on our own terms. It goes deeper by improving our sense of well being. Furthermore, when we have a stake in the community we live in, we participate more, making our neighborhoods safer and healthier for all members.

Not all the news about the housing market is negative, actually there are many great articles: “in defense of home ownership”, “ten reasons to buy a home “and “a dream house after all” to name a few. But regardless of where you stand on the housing market right now, we can all likely agree that there is no place like a home.

All of our experiences of home are unique. Please share your best memories of home.

Sellers: Making the Most of your First Impressions

As the old saying goes, you only have one chance to make a first impression. If you’re selling your home, it’s true, except that there are several impressions to be made, and each one might have its own effect on the unique tastes of a prospective buyer. I’ve worked with scores of buyers, witnessed hundreds of showings, and I can summarize that experience down this: a tidy and well maintained home, priced right, listed with professional photographs, enhanced curb appeal and onsite visual appeal will sell fastest. We all know first impressions are very important, but the lasting impressions are the ones that sell your home. It’s not easy, but if you can detach a little and look at your home from a buyer’s perspective, the answers to selling it quickly may become obvious to you.

The very first impression your home will make is through its web presence, whether on Windermere.com, the MLS, Craigslist or any multitude of websites. Fair or not, the price is typically the very first thing people look at, and it will be the measurement by which your home is judged. You can always adjust to the right price later, but the impact is lost. It will take something dramatic to get a buyer to reassess the way they feel about the value of your home.

Closely following price are the listing photos. According to this recent article in the Wall Street Journal, professional photos will not only impact your first impressions, it may also make a difference in the final selling price. Great photos might even overcome those initial price objections. Does the exterior photo capture your home at its hi-res best? Does the accompanying text enhance or distract? Online, your home has only a few seconds to capture the home buyer’s attention. If it doesn’t, they’ll click the “Back” button and resume their search. The goal is to have buyers excitedly calling their agents to arrange a showing.

Another old saying is “Location, location, location,” and sure enough, the first live impression of your home is the location. Forget this one; you can’t move your home. There’s not much you can do about location, right? Actually, there is one thing you can do: price it right from the start.

Let’s move on to the first time a buyer sees your home as they pull to the curb out front. Go stand out at the curb and look at it the way you would if you were shopping for a home. Sometimes, a couple hours of labor and $100 worth of beauty bark can be worth thousands in the sales price. I’ve had buyers choose not to get out of the car when we pulled up to a home that they had once been excited to see.

Likewise, I’ve had buyers say they’ve seen enough simply by peaking into the front door. The nose trumps the eyes when it comes to the first impression when entering the house. Buyers get more caught up in the details. Once the home shopper is inside, it’s easy for them to get distracted and focus on something that seems to have nothing to do with the structure they will be buying, from a dirty dish in the sink to a teenager’s bedroom that’s been decorated in posters and/or melodrama. Do everything you can to set a positive lasting impression. The buyer may look at dozens of homes. What is your strategy to convince them to make an offer on yours?

Guest post by Eric Johnson, Director of Education

Weatherizing your home: Protecting your investment through the harsh winter months

Posted in Living by Windermere Guest Author

It seems the winter is settling in early through much of the West Coast this year, with October frost and early winter warnings. Last week The Seattle Times reported, “This year will bring the most intense La Niña conditions since 1955 … Meteorologists say more rain, colder temperatures and bigger snowstorms are likely.” Whether the meteorologists are right this year or not, now is the time to do some home repair so you can enjoy the winter inside your warm house.

It seems the winter is settling in early through much of the West Coast this year, with October frost and early winter warnings. Last week The Seattle Times reported, “This year will bring the most intense La Niña conditions since 1955 … Meteorologists say more rain, colder temperatures and bigger snowstorms are likely.” Whether the meteorologists are right this year or not, now is the time to do some home repair so you can enjoy the winter inside your warm house.

Weatherizing your home should be more than just packing in your patio furniture, checking your furnace and cleaning out your rain gutters, though these make a big difference in preparing your home and avoiding December disasters. Weatherizing your home–especially in light of harsh warnings–will protect your investment from preventable damage, save money on energy costs and, most importantly, keep your home safe and warm for you and your loved ones throughout the winter season. Here is a useful checklist to manage your weatherization project.

Getting started: Check your toolbox to make sure you have all the materials you need for home maintenance in one place. This NY Times article provides a good list of the tools you’ll really need to maintain your home. After your toolbox is put together, you can confidently begin the maintenance on your home.

Insulation: According to the Sustainable Energy Info Fact Sheet “Insulating a home can save 45-55% of heating and cooling energy”. For the best results, your home should be properly insulated from the ceilings to the basement. However, if insulating your complete home is not in your budget, the U.S. Department of Energy states, “one of the most cost-effective ways to make your home more comfortable year-round is to add insulation to your attic.” By starting in your attic and progressively adding insulation to other areas of your home over time, you will avoid spending a large sum of money up-front.

Cracks & Leaks: Do a run-through of your entire house for cracks and leaks, from your roof to your baseboards. Winter weather is unpredictable. Whether your area gets rain, wind or snow, cracks in your house can lead to cold drafts or leaks that cause water damage. Do-it-Yourself.com reports, “The average house, even when well-insulated, contains cracks and gaps between building materials that add up to a hole about 14 inches square. All year long, a leaky house not only wastes energy, but can lead to water damage and provide a path for insects”. Depending on your house type, most cracks can be easily filled with supplies from your local hardware store in a do-it-yourself fashion. Use caulk to seal any cracks in the permanent building materials.

Windows & Doors: Another common place for heat leakage is in your windows and exterior doorways. Make sure seals are tight and no leaks exist. If you have storm windows, make sure you put them on before the cold season begins. This 5 minute video, How to Caulk Windows & Doors, demonstrates how to find leaks, pick the correct tools to use, and fill in the leaks. Don’t underestimate the difference some weather strips and a door sweep can provide in preventing drafts and keeping the heat in.

Rain Gutters: Clean your rain gutters of any debris. Buildup will cause gutters to freeze with ice, crack and then leak. Once you have removed the residue from the drains, test them by running hose water to make sure cracks and leaks have not already formed.

Pipes: Pipes are a number one risk in winter climates. A burst pipe can become a winter disaster in a matter of seconds. Remember to turn off your exterior water source and take in your hose. Internally, wrapping your pipes is a recommended precaution to take. This article from Insights, Natural Hazard Mitigation advises, “Vulnerable pipes that are accessible should be fitted with insulated sleeves or wrappings, the more insulation the better”.

Heating System: What is one thing gas fireplaces, wood burning stoves, and central air heating systems all have in common? They all need to be cleaned and maintained. Check and clean your indoor heating system thoroughly. This is important to avoid dangers such as house fires. If you use an old fashioned wood stove, make sure there is no leaks and that all soot build up or nests are removed. If a furnace is what you have remember to change the filters as recommended or clean out your reusable filters.

Fireplace & Wood burning stoves: Make sure to have chimneys and air vents cleaned early in the season if you are planning on warming your home with a wood-burning source. When your fireplace is not in use make sure to close the damper, some resources estimate an open damper can increase energy consumption as much as 30%.

Outside: As we mentioned before make sure you bring your patio furniture inside (or cover) for the winter- but don’t forget other, smaller items such as your tools, including a hose and small planting pot. These items can be damaged or broken in extreme cold. Clear out any piles around the side of your house, checking for cracks as you go so to avoid providing shelter for unwelcomed guests over the cold season.

If your property has large trees check for loose branches and call someone to trim back any items that may fall in your yard, on your roof or even damage a window.

Emergency Kit: Make sure your emergency kit is up-to-date with provisions, batteries, fresh water, food for animals, entertainment for kids, etc- especially if you live in an area prone to power outages.

When it comes to protecting our investments and our families’ safety “an ounce of prevention is worth a pound of cure” is a good philosophy. Your winter preparedness plan will fit your property, schedule and needs. What are some tips you have for preparing for winter? What are some of your favorite activities to do at home over the winter while weathering out a storm?

By Brittany Lockwood

You may know Brittany as the helpful voice behind the Marketing Solutions Help Desk. She grew up in Cheney, Washington so she knows a thing or two about harsh winters.

The First Decade

Posted by Geoff Wood

The other day I was searching for my daughter’s cell phone number – which I haven’t memorized because I simply speed-dial it – and I realized it’s been years since I memorized anyone’s phone number. And this was just after I’d booked a flight online and selected my seat, and downloaded some new music into my iPod.

It occurred to me that these are just three examples of the tremendous changes that have happened just since the new millennium began. At the beginning of this decade, iTunes, YouTube and Facebook did not exist. Today, their combined daily views and downloads are in the billions.

An article in Newsweek a few months ago highlighted how much things have changed in a decade. The numbers are staggering and surprising.

-

- Ten years ago, a total of 400,000 text messages were sent per day; today 4.5 billion are zinging through cyberspace every day.

-

- In 2000, 12 billion emails were sent each day; today 247 billion are sent daily (many of which were in my spam filter this morning).

-

- Ten years ago, about 208 billion letters were mailed through the postal system each day; today the number of letters mailed daily is less than 176 billion.

This decade has been tumultuous, to say the least. Beyond the tremendous technology-driven advances, we are still struggling with this economy. Unemployment rates are too high. Banks are still struggling. And it is heartbreaking that people have lost their homes.

Even though there is a lot of uncertainty, I remain optimistic. I am realistic enough to know that this recovery will take awhile. But recover we will.

One thing that hasn’t changed in the past decade is the resiliency of real estate over time. When you look at median single-family home prices ten years ago versus this year, you’ll see that home values have increased since 2000. This is encouraging, especially when you consider that the stock market today is the same place it was 10 years ago. For most people, their home is worth more today than when they bought it. It might be worth less than it was two or three years ago, but real estate has never been about day trading. It’s a long-term investment. And if the last 10 years, or 100 years, are any indication, we can count on growth in home values.

And that’s a good thing.

July Median Home Prices*

2000

2010

National

$151,100

$182,600

*Source: NWMLS

What are some of the most memorable changes for you in the past decade?